Breaking Free: Unleashing the Power of Captive Insurance

Captive insurance, specifically within the framework of the IRS 831(b) tax code, has emerged as a revolutionary way for businesses to regain control over their insurance needs. Traditionally, companies have relied on third-party insurance providers that often come with limited coverage options, high premiums, and a lack of flexibility. Enter captive insurance, a concept that flips the script and puts businesses in the driver’s seat.

At its core, captive insurance refers to the practice of forming an insurance company, or "captive," that is wholly-owned by the insured business. This means that instead of depending on external insurers, companies can create their own insurance entity that tailor-fits policies to their specific needs. By doing so, businesses can minimize risks, enjoy broader coverage, and have greater control over claims processes.

Captive Insurance

One of the key features of captive insurance is its potential financial benefits, particularly under the IRS 831(b) tax code. This code offers tax advantages to smaller captives, known as microcaptives, with premium income of up to $2.3 million. By qualifying under this threshold, microcaptives can be taxed only on their investment income, rather than their premium income, leading to potential tax savings for businesses.

With the power of captive insurance, companies can break free from the constraints of traditional insurance models and create a strategic risk management tool that aligns with their unique needs. From industries ranging from manufacturing to real estate, businesses are embracing the captive insurance revolution and harnessing its potential for greater financial control and security.

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. Readers are advised to consult with appropriate professionals before making any decisions.

Understanding Captive Insurance

Captive insurance, also known as microcaptive insurance, is an alternative risk management strategy that has gained popularity in recent years. It is governed by the IRS 831(b) tax code, which provides certain tax advantages for small captive insurance companies.

In simple terms, captive insurance involves the creation of an insurance company to cover the risks of a parent company and its affiliated entities. Unlike traditional insurance, where premiums are paid to a third-party insurer, a captive insurance company is owned by the parent company and serves as its own insurer. This allows the parent company to have greater control over its insurance program and potentially enjoy financial benefits.

One of the key motivations for utilizing captive insurance is the potential tax savings it offers. Under the IRS 831(b) tax code, small captive insurance companies can elect to be taxed only on their investment income, rather than on their total premium income. This can result in significant tax advantages for qualifying companies.

However, it is important to note that captive insurance is a complex area of insurance and tax law, and it may not be suitable for every business. Before considering captive insurance, it is advisable to consult with qualified professionals who can assess its feasibility and provide guidance on its implementation.

Overall, captive insurance presents an intriguing opportunity for businesses to take greater control over their risk management strategies and potentially enjoy tax advantages. By understanding the intricacies of captive insurance and working with knowledgeable advisors, businesses can explore this alternative risk management approach and potentially reap its benefits.

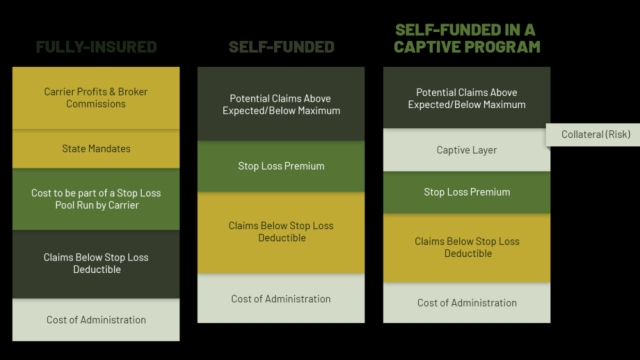

The Benefits and Advantages of Captive Insurance

Increased Control and Flexibility

Captive insurance provides businesses with increased control and flexibility over their insurance programs. By forming their own captive insurance company, companies can tailor coverage to their specific needs, rather than relying on traditional insurance policies that may not fully address their unique risks. This allows businesses to have better control over their insurance costs and coverage, reducing the potential for underinsurance or overinsurance.

Potential Cost Savings

One of the key advantages of captive insurance is the potential for cost savings. Through a captive insurance arrangement, businesses can retain a portion of the risk and potential insurance profits that would typically go to a conventional insurance provider. By effectively managing their own insurance risks, companies can potentially reduce premiums, take advantage of favorable tax treatment, and achieve long-term cost savings.

Customized Risk Management

Captive insurance offers companies the opportunity to implement customized risk management strategies. With a captive, businesses can align their insurance policies with their overall risk management objectives and company-specific needs. This allows for greater flexibility in underwriting policies and procedures, claims management, and loss control. By tailoring their captive insurance program, companies can create a comprehensive risk management solution that aligns with their unique risk profile and business goals.

(Note: This is the end of Section 2 of the article. Refer to Section 3 for further information on captive insurance.)

Navigating IRS 831(b) Tax Code

When considering captive insurance, it is important to understand the specific regulations outlined in the IRS 831(b) tax code. This code provides guidelines and requirements for microcaptives, which are insurance companies formed by businesses to insure their own risks.

The IRS 831(b) tax code offers certain advantages to microcaptive owners. One key benefit is the ability to elect for favorable tax treatment. Under this provision, qualifying microcaptives can be taxed only on their investment income, rather than their underwriting income. This can lead to significant tax savings for businesses, making captive insurance an attractive option.

However, it is crucial to note that the IRS has implemented strict criteria for microcaptive eligibility. The requirements include having sufficient risk distribution, maintaining arm’s length transactions, and conducting legitimate insurance activities. These guidelines are in place to prevent abuse of the tax benefits and ensure that microcaptives operate as legitimate insurance entities.

Navigating the IRS 831(b) tax code can be complex, and it is essential to consult with experienced professionals who specialize in captive insurance. They can help ensure that your microcaptive structure complies with all relevant regulations, maximizing the potential tax advantages while avoiding potential pitfalls. By understanding and adhering to the requirements of the 831(b) tax code, businesses can better harness the power of captive insurance for their risk management strategies.

Recent Comments